At the onset of the year, we (Arca) released our annual digital assets predictions which focused on a few themes that we believed would ultimately drive the majority of digital asset investment gains in 2020. We obviously did not anticipate COVID-19, a 35% jump in the M1 money supply, or the accompanying acceleration of an already ongoing shift from a physical world to a digital world, but our predictions proved fairly accurate nonetheless.

This post is part of CoinDesk’s 2020 Year in Review – a collection of op-eds, essays and interviews about the year in crypto and beyond. Jeff Dorman, a CoinDesk columnist, is chief investment officer at Arca where he leads the investment committee and is responsible for portfolio sizing and risk management.

With 2020 concluding, it’s time to look back at how these predictions fared, and touch on a few important drivers of returns in 2020 that we did not foresee. The shift to digital is only getting started, and it is therefore highly unlikely that anything will change once the world re-opens.

Post Mortem of 2020 Predictions

Prediction #1: Thematic investing will drive digital asset performance, specifically in the following areas: Rewards, Structured Tokens, Staking, and DeFi.

Thematic investing has unequivocally driven returns in 2020, and three of the four themes we identified have proven accurate. The outlier was the staking theme, which was not a large driver of YTD returns. In fact, most of the tokens that operate under “proof of stake” consensus have underperformed the market this year.

However, the reason for this underperformance can largely be attributed to the success of our other three identified themes. The growth of decentralized or open finance (DeFi) and the newfound focus on structuring tokens with real value accrual mechanisms and yields, driven primarily by user rewards, has made staking for yield somewhat obsolete from an attractive investment standpoint.

See also: Jeff Dorman – Digital Assets Are More Recession-Proof Than You Might Think

Let’s start with DeFi. This sector of the market has been hands down the runaway leader in digital assets, from both a growth perspective and a returns perspective. Our prediction was quite simple:

Decentralized Finance is still tiny, but it is growing quickly and will likely be a major growth engine in 2020. Conversely, a ton of value has already accrued to centralized finance (CeFi) companies – Coinbase, Binance, Celsius, Deribit and BitMEX – and this market is getting very saturated. We believe DeFi will be the “growth sector” of 2020, while CeFi will be a “value sector.” As such, a blind basket of DeFi tokens will likely do very well regardless of which tokens you own, whereas in CeFi only one or two companies will win out and grow at the expense of others.

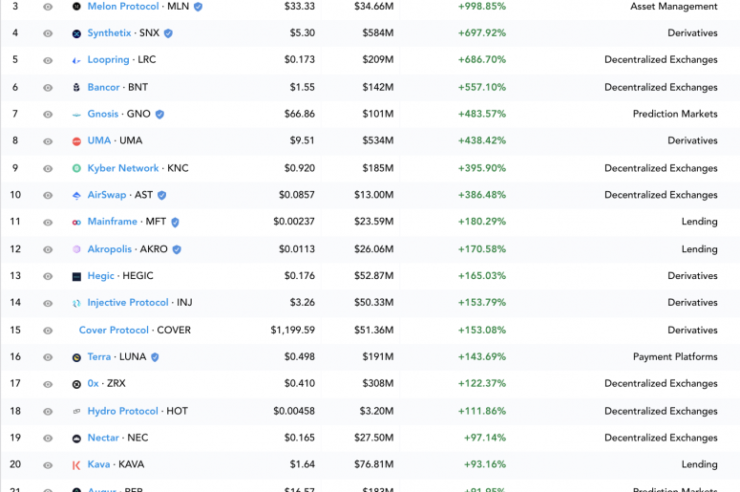

Digging deeper, decentralized trading exchanges (DEXs) have been one of the most impressive sub-sectors, posting all-time record high volumes, but we’ve also seen strength and growth coming from asset management protocols, synthetic assets, lending/borrowing platforms, and insurance. A basket of diversified DeFi tokens across insurance (NXM), asset management (YFI, MLN), DEXs (KNC, RUNE, SUSHI, UNI), lending/borrowing (AAVE), and derivatives (SNX) created the strongest subset of returns across any other sector of digital assets.

Moreover, the strong DeFi returns did not stem purely from platform growth. Much of it can be attributed to our other prediction, “structured tokens and enhanced tokenomics.” The flexibility of token structures has allowed token issuers to change the rules and enhance the features that come with owning a token and participating in the network. While this can be scary from a legal standpoint since you don’t always know exactly what you are getting at the time of investment, it’s also invigorating from an investing standpoint because it allows good teams who issue tokens to continue to tweak the value accrual model until they get it right.

And boy are they ever. From Compound (COMP) and the liquidity mining revolution, to Synthetix (SNX) and its velocity sink, to Uniswap (UNI) and its fair decentralized launch, to revamped incentive structures rewarding governance at Kyber (KNC) and Aave (AAVE)… token issuers are scrambling to introduce new models that enhance the value for both users and investors. We applaud this evolution.

Prediction #2: Sports and other live events will play a huge part in blockchain’s success as the “live, in game experience” will be enhanced via digital tickets, voting rights, and player engagement.

We had no idea that sports would be shut down in 2020, but I’m not sure it would have changed the outcome. Our thesis regarding the “digitization of the fan experience” was taking form with or without the ensuing lockdown. The in-game experience was already dying at the hands of interactive, at-home engaged fan experiences, and COVID-19 was simply the nail in the coffin.

We went into great detail discussing “Fan Engagement Tokens” (FTOs) from Socios (CHZ) earlier this year, and the successful issuance of digital assets tied to voting rights and decisions affecting major sports clubs. We’re also seeing a rise in digital baseball cards and digital collectibles as well as tokens backed by the salaries of athletes.

Additionally, the “digitization of the fan experience” is extending beyond sports into other areas like music and entertainment. While there are not a lot of pure play ways to express this theme yet today, we continue to expect more opportunities to come in the near future.

Prediction #3: More M&A, the Bitcoin halving matters, and existing non “crypto-native” companies will issue tokens.

Let’s check in one-by-one to see how we did:

More mergers between pick & shovel companies, often at distressed levels.

From Coinbase assuming Tagomi, to Binance going on a spending spree, to Voyageur acquiring LGO, M&A is in full force as the leading service providers take advantage of the oversaturation of smaller platforms that never achieved solo success. Several of these transactions were more takeunders than takeovers given the lack of progress or success of the acquirees. We did not anticipate the recent wave of DeFi “fake-quisitions,” but are encouraged by the idea of combining user bases and developers to build DeFi conglomerates.

The Bitcoin halving, while telegraphed and understood, will still be a huge driver of digital asset growth.

While the halving itself, as expected, did basically nothing for Bitcoin’s price in real-time, the consistent monetary policy and limited fixed supply has attracted new players, and once that happened, we are now witnessing a supply shortage. From Paul Tudor Jones to Jim Simons, and more recently MicroStrategy, Square, Stan Drukenmiller and more, the cavalry is clearly coming and they are fighting over a small pie.

Existing non-crypto native companies will utilize tokens.

While this is being held back by a lack of regulatory clarity and a lack of investment bankers, it’s happening, slowly. For example, both Reddit and Atari issued tokens. While these are just small examples, the world is beginning to recognize that tokens can be utilized in a company’s capital structure as complements to debt and equity.

We expect more of this in 2021 and beyond, as every company with a subscription model (Netflix, ESPN, gym memberships) or a consumer customer model (restaurants, airlines, internet shopping) will recognize that tokens are the greatest capital formation and customer bootstrapping incentive mechanism we’ve ever seen.

What did we miss in 2020?

We’ll be out soon with our 2021 predictions, many of which stem from budding 2020 events that we either did not foresee, or grew faster than anticipated. A few things that we have our eye on:

- Bitcoin has graduated from “digital assets playground” to “mainstream global investment.” Investors now have the knowledge and means to buy Bitcoin themselves, and we are seeing it in real-time, which happened quicker than we anticipated. Very soon, investors will specifically seek out digital asset hedge fund strategies that don’t own any Bitcoin, as they want fund managers to give them exposure to assets that they can’t buy themselves, or don’t know exist. As a result, there is a good chance that actively managed hedge funds and passive indexes built around high allocations to Bitcoin have a very short shelf-life.

- Banks and broker/dealers are scrambling right now to “cover Bitcoin” – meaning research on publicly traded securities like GBTC, MSTR, Hut 8, SQ, GLXY and pretty soon the anticipated IPOs of Coinbase and Digital Currency Group (CoinDesk’s parent). Soon, these banks and BDs will realize the real opportunity is investment banking fees from underwriting new tokens issued by traditional companies rather than trying to extract a piece of the Bitcoin trading pie.

- We anticipated a rise in DeFi, but not to the extent and degree with which it occurred. Decentralized governance is now less about ideology or risk transfer, and more about capitalism. Historically, there has been nothing in digital assets worth governing, but now DeFi protocols are generating real revenues, and that is worth fighting over. While 2017 tokens were about fundraising a dream, 2020 and beyond tokens are about aligning incentives amongst stakeholders (founders, developers, customers), and tokens are proving to be the best instrument for fostering this growth.

- Community issued tokens (LINK, CEL, SUSHI, YFI) are growing faster than VC-backed tokens (COMP, ATOM, FIL, UNI). This not only suggests that the reliance on VCs may be reduced, but it also may have structural consequences. To date, “show me” stories with high upside but low probability of success have dominated the digital assets landscape, but as VC-backed pipe dreams dissipate, we may see a resurgence of value – those tokens issued by projects and companies that are already having success rather than those that might one day grow into success.

After a whirlwind 2020, we look forward to seeing what 2021 holds.

{kind=link}

{kind=link}

Comments (No)