The good news is America is not in the midst of a full-blown civil war – not yet, at least.

But, however you feel about Joe Biden’s apparent victory in the most difficult presidential election in living memory, you’d be foolish to believe all is well in this country. Four years after Donald Trump rode a wave of white suburban discontent to a shock victory, and with the echoes of this year’s Black Lives Matter protests still resonating, the vitriol and conspiracy theories generated by a starkly divided vote suggest trust in the U.S. system of government is cratering.

Why? Well, as a starting point, the American Dream has been decimated by the disruptive forces of globalization and digitization. Huge swaths of society, many concentrated in the so-called Rust Belt of the Midwest, no longer believe the future will be brighter for them or their children.

That stirs up the same-old 20th century ideological arguments for getting the Dream back. (The left wants to tax the rich and widen the safety net for the middle class while the right says that’s socialism and that it will halt job creation.)

But there’s a more fundamental problem here: governance itself is broken. Too many people feel they have no agency, their voices aren’t heard, they have no means to shape policies that are dictated by vested interests.

We need a system designed for a globalized economy and an internet-connected society, one that favors transparency, accountability and efficiency, and which mitigates the influence of hidden, vested-interest money. We need to address the principal-agent problem.

This column is most definitely not going to say “blockchain fixes this.” But it will draw on a guiding CoinDesk maxim, one coined by Executive Editor Marc Hochstein: “Blockchain doesn’t have all the answers but it asks the right questions.”

Applying the lens of decentralization and programmable contracts to big societal issues can help expose where current thinking is wrong. It can reveal how centralized control of information and transactions enables powerful interests to influence policy and, in so doing, undermine the free market. And it helps us think creatively around how new open-information and incentive models might address those problems.

It doesn’t mean “put it on a blockchain.” (And definitely not blockchain voting – bad idea.) It means thinking outside the box.

In our weekly Money Reimagined podcast, Sheila Warren and I talked to two outside-the-box thinkers on their ideas for improving governance.

Quadratic voting and open auctions

One of our guests was Glen Weyl, the political economist and Principal Researcher at Microsoft Research New England, who co-authored the book “Radical Markets” with University of Chicago Law School professor Eric Posner. We chose to focus on just two of the many ideas that that book puts forward.

One is quadratic voting, which allows people not only to vote for or against a particular issue but to express how strongly they hold that view by buying extra votes – up to a certain limit of assigned credits. The cost in credits of each additional vote increases by a quadratic formula. It’s designed to help small groups of voters who care deeply about particular issues while still constraining them from overly skewing results.

Weyl has also worked on a variation of the concept with Ethereum founder Vitalik Buterin called quadratic funding, which in theory could diminish the influence of wealthy “whales” in voting systems that are based on financial holdings or contributions.

The second big idea we explored is that of perpetual open auctions. Here, every bit of property, including what we might otherwise think of as public property, is owned by private entities with the proviso that it is always up for auction and that the majority of the value created from it is shared equally among citizens as a social dividend.

Weyl and Posner argue that such an arrangement would incentivize owners to manage the property well, and that the wider distribution of wealth creation would give a greater number of people the wherewithal to start businesses. It would also be easier to develop land for infrastructure, such as high-speed rail lines, because the developer could easily acquire it.

Both of these ideas are rooted more in legal and process innovation than in software and distributed computing per se. But they intersect nicely with concepts associated with the crypto and blockchain space.

One is the potential for self-sovereign identity models to prevent people from gaming quadratic voting. Another is the potential enhancements that smart contracts, non-fungible token-based property, and decentralized finance (DeFi) concepts such as automated market-making might bring to open auctions. Also, quadratic funding might fix free-rider problems in blockchain projects, Buterin believes.

Smart taxation

Our other guest was Jeff Saviano, the global lead of tax innovation at EY. He is a member of the Prosperity Collaborative, within which organizations such as the World Bank, MIT Media Lab’s Connection Sciences lab and the New America Foundation are working with governments to improve transparency and efficiency in the collection and distribution of taxes.

Saviano talks of how blockchain-based tracing systems might not only give taxpayers a transparent view of how their taxes are being spent but also incorporate programmability.

For example, the actual, uniquely identified dollars that you contribute could be channeled directly and transparently into identifiable services that immediately benefit you and your community. Or, governments could use smart contracts to put hard constraints on those dollars, so only certain categories of expenditure, and not others, are enabled.

Restoring the social covenant

Whether these ideas work or not, policymakers must restore the social covenant between those who govern and those who are governed. And that comes down to trust.

We are the principals in this relationship. As our representatives, government leaders are supposed to be our agents. But if there is insufficient trust in them, people instead see them as competitors.

As has been seen in countless failed states, a vicious, self-fulfilling cycle can arise. People avoid paying taxes so as not to feed the kleptocracy, which starves the state of the resources it needs, encouraging more corruption and theft by police and other employees of the state.

The endgame in all that is a collapse in the most important expression of the state’s relationship with its people: its currency. The hyperinflation seen in Latin American countries such as Argentina, Brazil and Venezuela can be thought of as a manifestation of the collapse in the social covenant.

It’s worrying to think similar breakdowns may be underway in western nations, including the U.S. While there are currently no big inflation risks in the benchmark Consumer Price Index, these kinds of concerns underpin this month’s sharp rally in bitcoin, which burst through $15,000 on Thursday.

Buying bitcoin is one way for people to protect themselves from future governance failures. But it’s more important that we find solutions to prevent those failures.

Did prediction markets fail their big test?

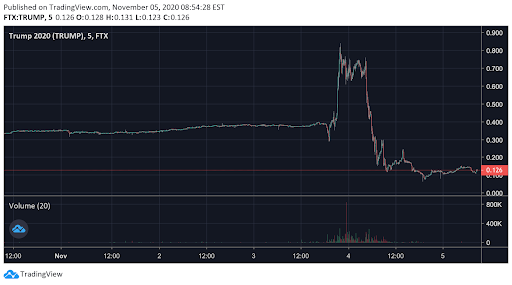

Around 9 p.m. ET during the early vote-counting phase of the U.S. election on Tuesday evening, the value of the Trump futures contract on FTX crypto derivatives exchange dramatically surged higher. As you can see in the chart below – a five-day snapshot taken on Thursday morning from the FTX website – the value of the contract doubled from about $0.40 to $0.80 at that time. FTX was then assigning an 80% probability to President Trump winning the election. Early Wednesday morning, an even more dramatic change happened: The contract’s value plunged all the way down to around $0.12, which is more or less where it stayed.

There’s an easy explanation for this relatively short-lived spike. Early results on Tuesday showed some strong numbers for President Trump, especially in the vital battleground states of Michigan, Wisconsin and Pennsylvania, and there was not yet any data on the shift that would later go toward Joe Biden once early-voting and mail-in ballots were counted. Suddenly, expectations had changed from what the FTX market and other prediction markets such as PredictIt had been saying in the days beforehand, when Biden was forecast to win.

All through the week, politicos had been warning about the “red mirage” effect, where the early count would favor Trump because more of his voters were expected to vote on Election Day whereas Biden vote would skew toward early or mail-in votes, which were to be counted later. We were repeatedly told to be patient, that we were in it for the long haul. All this was, in other words, predictable ahead of time. In short, neither the rally or the subsequent sell-off should have happened at all.

So much for the “wisdom of the crowd.” So much for prediction markets.

It seems all FTX did on Tuesday evening was to enable speculators to take short-run bets on people’s herd instincts during the hyperbole of election-night TV commentary.

This was supposed to be prediction markets’ coming-out moment. The most high-profile election of all time and tight polling made for a big chance to show off what the new crypto-based versions of an old idea could do. Instead, we got further evidence to back up past results showing prediction markets don’t work well.

The global town hall

BITSTRATEGY. One person no doubt pleased with bitcoin’s price surge over $15,000 is Michael Saylor. In separate transactions in August and September, the CEO of investment advisory firm MicroStrategy shifted a total of $425 million worth of the company’s cash on hand into the dominant cryptocurrency. The move turned Saylor into a rock star in crypto circles, set off some copycat measures by other companies such as fintech provider Mode Global Holdings and payments service Square, and stirred a debate on whether bitcoin is a viable treasury-management asset for companies looking to protect the purchasing value of their cash.

Veteran Wall Street Journal columnist Jason Zweig wasn’t impressed, though. An otherwise balanced analysis of Saylor’s move ended on this note:

“…MicroStrategy is no longer just a software company. Now it’s a bitcoin bet. Investors who wish to buy bitcoin could always do so themselves with the proceeds of a dividend or share buybacks. The point of buying a stock is to get a stake in a business, not to take a flier on cryptocurrency.”

It’s a clever line, but in the face of the improvement in bitcoin’s price Saylor could equally argue that he’s achieved what he needs to do. He legitimately sees a decline in the dollar’s purchasing power because even though the benchmark measure of the consumer price index is stable to low, there are rising prices in asset markets, in food and commodities. This was a hedging strategy for a time of great uncertainty and, as anyone who’s tried to run a business in the middle of a crisis will tell you, a necessary one. Sometimes the need to survive is more important than running the underlying business activity. You have to make smart decisions around cash on hand.

Yes, Saylor could have launched a share buyback to return value to stockholders, but doing so would leave less room for maneuver with cash on hand in the future (should an acquisition target come along, for example) and would continue to tie the company’s valuations to a fiat valuation he believes will be depleted in purchasing power terms. So, it really comes down to whether or not you believe there’ll be long-term inflation.

I’m looking forward to chatting with Saylor next week when he joins our “Bitcoin for Advisors” event for registered financial advisors.

GOING IT ALONE. Andrew Browne, another veteran financial journalist, also formerly of The Wall Street Journal and now at Bloomberg, took a look at China’s new policy of “self reliance.” Somewhat alarmingly, the phrase, which was inserted into Xi Jingping’s new five-year plan, stems from Mao-era rhetoric. But as Browne points out, it’s unlikely to mean China is closing its doors and may even end up making its economy more open and less isolationist. The reality is the kind of policies Xi’s government will need to pursue to give greater emphasis to its domestic economy and reduce China’s reliance on foreign export markets will require it to further open up to foreign service firms, especially in the field of finance.

Browne doesn’t mention capital controls. But any talk of liberalizing financial services to better serve domestic consumers and businesses inevitably leads to that question, because to grow such businesses with foreign help there needs to be a more free-flowing interest rate market, which in turn requires a more open flow of capital in and out of the economy.

One big question is, what does this mean for cryptocurrencies? Would looser capital controls put the yuan under pressure and favor bitcoin, or would that lower the appeal of bitcoin, which has been used by Chinese nationals to bypass those restrictions?

Another question: How does this tie into China’s new digital currency, the digital currency electronic payments (DCEP) system? Lowering capital controls might signal a path to making that currency available in offshore markets or as a payment rail in overseas supply chains such as those expected to operate over China’s One Belt One Road network. But probably more important though less obvious to observers obsessed with China’s geopolitical strategy is that “self reliance” is consistent with the heavy investment the country is making in integrating technologies such as the DCEP with its Blockchain Services Network to boost the performance of its domestic economy.

Tying those in with a host of data-driven Fourth Industrial Revolution developments could give China an advantage in its competition with the U.S.

Relevant reads

Square Reports Over $1B in Quarterly Bitcoin Revenue for First Time: Q3 Earnings. Something that’s going to be quite different about this bull run in bitcoin from the last one three years ago is it will be accompanied by upbeat earnings reports from mainstream companies with exposure to it. We discussed MicroStrategy above. This news, reported by Brady Dale, is from Square. Worth noting is that what’s good for Square shareholders isn’t necessarily good for its customers, as these revenues represent the fees they are paying for using a payments technology that, in theory, should be middleman-free.

US Seized More Than $1B in Silk Road–Linked Bitcoins, Seeks Forfeiture. It’s the bitcoin crime story that will never go away. U.S. agents seized some $1 billion worth of bitcoin they say was earned by the shuttered Silk Road drug market. The massive stash was forfeited by an unnamed hacker who had stolen the bitcoin from Silk Road. The report raises more questions than it answers – such as, what involvement did jailed Silk Road founder Ross Ulbricht play in all this? Kevin Reynolds reports.

Ethereum 2.0 Countdown Begins With Release of Deposit Contract. It’s hard to keep track of all that happened in this past, busy week of news. This one would have been a much bigger story if it weren’t for the bitcoin rally and the return of Silk Road: the first big step in Ethereum’s long-awaited, highly complex migration to its new proof-of-stake architecture. CoinDesk reporter Will Foxley has been all over this. He reports on the deposit contract by which a group of market participants will lock up their existing ether funds in return for the right to own a new version of ether that will operate within a parallel proof-of-stake network.

In the CBDC Race, It’s Better to Be Last. In a contrarian take, CoinDesk columnist JP Koning – one of the first people to envisage a central bank digital currency with his “Fedcoin” idea in 2014 – is now saying the U.S. can afford to take its time. While others worry American tardiness will put it at a disadvantage to China’s fast-moving digital currency, Koning says that because, like all central banks, the Federal Reserve is a de facto monopoly, it need not worry about competition and can instead afford to wait. I disagree, but if you’re a regular consumer of Money Reimagined, you’d already know that. Koning, as always, is a good read.

{kind=link}

{kind=link}

Comments (No)