Cryptocurrency is becoming increasingly mainstream. Between the entrance en masse of traditional financial institutions — from investment funds, to banks, to insurance companies — to the multitrillion-dollar market capitalization, crypto is truly unignorable.

As such, it is also increasingly on the radar of regulators around the world, particularly in the United States. How can this industry balance stability and investor protection on the one hand with the promotion and support of innovation on the other?

There are three paths to regulating crypto. The first is to not regulate it as much, but given the incredible growth and increasing overlap with traditional financial markets, it is unlikely that regulators will find that path tenable.

Another option is to regulate the industry from on high, without deep engagement or consultation from good-faith companies in the crypto space. This way could be perilous and could sacrifice the powerful financial innovation of blockchain that could be harnessed for good.

The third — and we believe the only truly viable option — is regulation that involves an ongoing partnership with the industry itself. Many in the crypto industry already see this sort of proactive, innovation-oriented regulation as something that will greatly advance the industry.

Related: Blockchain will thrive once innovators and regulators work together

Bitcoin regulation in historical context

Bitcoin (BTC) was born over a decade ago as a peaceful protest against the expansive monetary policy of the great financial crisis of 2008. What started as a niche industry for cyberpunks, libertarians and, quite frankly, people wanting to buy weed more conveniently and anonymously has morphed into a concentration of mind power, with 46 million Americans owning Bitcoin. The sheer scale of crypto as an asset class, with a market capitalization peaking north of $2 trillion, puts it on the radar of every lawmaker and regulatory agency in the world. To expect crypto to march onward in the unsupervised manner of its early years is simply unrealistic. Mainstream asset classes cannot go unnoticed, and the influx of new investors needs protecting.

Related: Europe awaits implementation of regulatory framework for crypto assets

As entrepreneurs, our concern about regulation does nt stem from a desire to run amok. If history is any guide, too often the regulation on innovative businesses is imposed by legislators who are, quite understandably, not into the intricate details of industry-native processes and have little or no practical experience. This gap between innovators and regulators opened up decades ago with the massive expansion of internet-based companies, and has resulted time and again in unnecessarily burdensome rules that do little to serve their purported purpose. The alternative is of no benefit to advanced jurisdictions because nimble companies will usually seek offshore tax havens with little regulatory friction and lax rules, which ultimately hits state coffers, especially in post-COVID-19 remote-work-adjusted societies. The reality is: Legislation lags behind innovation, which occurs at a significant pace.

The matter gets even more complicated when one considers the decentralized finance (DeFi) space. These solutions, colloquially referred to as “noncustodial” or “unhosted” — meaning there is not a centralized third-party intermediary, but the intermediary is the software itself — present challenges when it comes to putting them into existing rules, especially in financial intermediation and securities laws.

Related: Authorities are looking to close the gap on unhosted wallets

CeFi as bridge between DeFi and regulation

Our hypothesis is that the most productive legislation will come from regulators working with good-faith actors in the crypto space who wish to actively engage with them. What does that engagement look like? One part of it is taking proactive steps to work within the existing regulatory frameworks in order to better identify where gaps and friction remain.

To take the example of DeFi above, while it presents new regulatory challenges, there are ways to ease this burden initially. Centralized finance (CeFi) companies can be the interim solution, serving as a bridge between the traditional financial sector and the regulatory framework that encapsulates them on one hand and the decentralized finance space on the other. These companies very well understand the sector from both the infrastructure point of view and the needs of their users.

Until we reach the conclusion that the current regulatory framework does not apply for blockchain companies or the sector gets specific legislation, CeFi businesses have been on a license acquisition crusade, culminating in a significant number of licenses from regulators across the globe, with more pending authorizations in the pipeline. This means that they are perfectly placed to allow DeFi projects to piggyback on our infrastructure, as they are just starting to consider allocating funds to legal expenses and lobbyism.

Also, they can rely on established Know Your Customer (KYC)/Anti-Money Laundering (AML) procedures prescribed by the Financial Action Task Force (FATF), as well as fiat on- and off-ramps to broaden their offering and bring it to their users in a manner that is compliant with the incumbent rules.

Related: FATF draft guidance targets DeFi with compliance

Key concerns of regulators and how the industry can help

If one part of being an engaged partner to regulators is seeking to work within existing frameworks first, another part is having a perspective on key areas of legitimate concern for regulators, so they can work with industry rather than against it to develop solutions.

Crypto is volatile. Despite being in a downward trend, volatility is here to stay. As a disciple of Benoit Mandelbrot and a student of capital markets, let me tell you: Volatility tends to cluster — i.e., volatility begets more volatility. This is what attracts many people to the space — the promise of multiple X on their initial capital. Of course, volatility works both ways. Yes, Bitcoin can go up 15x in 12 months, but it can also undergo corrections of 30% in a matter of hours. Such rapid, severe corrections occur in every bull cycle. However, it just so happens that those corrections usually precede larger legs up, as the March 2020 crash showed.

The more recent correction of May, while not as severe, was important because it showed the remarkable resilience of the DeFi space. There were cascades of liquidations, yet the protocols stood their ground (for the most part) and performed as designed even as Bitcoin slumped 35% and Ether (ETH) close to 40%, futures traded in severe backwardation, and implied volatility in the options market surpassed 250%. In my former life, I was a trader in equities futures, and I have vivid memories of the S&P 500 flash crash of May 6, 2010, where the indexes lost 10% within minutes, only to retrace those losses a short period after. It was anything but orderly as the most advanced, sophisticated, regulated and monitored markets experienced total mayhem. It took five months for the Securities and Exchange Commission and CFTC to gain a preliminary understanding of what actually happened.

It is also worth noting that despite the May correction, Bitcoin is up 27.26% in 2021 and has surged 284.58% over the past 12 months. Meanwhile, the S&P 500 has added 11.95% year to date and 34.63% over the past year. Gold is flat for the year and has gained 11% in the past 12 months. In short, much of the volatility concerns around Bitcoin have to do with one’s time scale — and moreover, the investment strategies one is using.

Within this overall framework of volatility, there is one aspect worth discussing further: leverage.

As the best-performing asset of the past decade, Bitcoin is unique in many aspects, and investing requires a certain mindset and the right time horizon. Day trading any asset — but even more so, cryptocurrencies — is a one-way ticket to obliterating your trading account. 100x, 135x and 500x leverage means you get liquidated when the underlying asset moves less than 1%, which in crypto might mean seconds. Here’s a great thread on volatility and cascades of liquidations. Spoiler alert: Although objective and informative, it comes from someone who profits enormously from excessive leverage.

Bitcoin and other crypto assets are a great addition to any well-diversified portfolio and should be bought and holded for extensive periods of time during which, history has shown, Bitcoin has outperformed every other asset, except perhaps the U.S. dollar against the Zimbabwe dollar. Should you put your kid’’ college funds in crypto after it has 15x-ed in 12 months? Probably not. And definitely not with any sort of leverage, as even 2x leverage can get you liquidated in a March 2020 sort of correction, which saw intraday prices dip more than 50%.

Related: Risk management in crypto: Aka ‘the art of not losing all your money’

At our company, we have little tolerance for leverage and have been advising our extensive customer base to be cautious since at least January. A client depositing $100,000 worth of Bitcoin gets an instant crypto credit line of $50,000 with us. Compare that to a trading platform that allows traders to enter trades with 100x leverage. That means, in order to buy a position of $100,000 in BTC, the margin required is $1,000. The rest of the $99,000 is borrowed at rates that are lucrative for the lender. Additionally, exchanges and prop shops profile their clients — they are quick to identify those high-rollers engaging in 100x levered trades, then they gladly take the other side of the trade, as everything these clients deposit can instantly be booked as profit.

In our opinion, leverage in the crypto space would be a reasonable place for regulators to look when analyzing who is focused on investor protection. The legitimate purpose of protecting investors in nascent industries is a difficult balancing act, as it sometimes borders on the stifling of innovation. But the reverse is true as well: “Innovation” cannot be used as an excuse for rapacious behavior because 100x leverage is not innovation. Forex got it pre-Satoshi, and no, it does not contribute to the betterment of society.

Companies need to work with their respective national bodies to ensure the right type of investor protection legislation is implemented. This approach is far more constructive than the alternative: stubbornly insisting that the current regulatory framework is obsolete and doesn’t capture the cutting edge of crypto and fintech.

Crypto and money laundering

On money laundering, most crypto industry participants have the same feeling: On one hand, we are happy to play by the rules. On the other, crypto has been unfairly maligned when the massively preferred currency of money laundering has been and remains the U.S. dollar.

Any widely accepted currency is prone to money laundering, and the fact remains that the incumbent financial system and the U.S. dollar are the preferred means for illicit purposes. It is not just about the medium of exchange itself. Do the rewards of aiding the finance of illicit activities outweigh the repercussions? Just type in your search engine the name of a major bank plus money laundering and you will see how large the problem is. Then try to find out how many of the complaints were civil vs. criminal, and what percentage ended up with settlements with “no admission of guilt.” As long as a slap on the wrist and a few percentage points of the gains from abetting illicit activities remains the punishment, there is little to no hope that money laundering will suffer any significant blow.

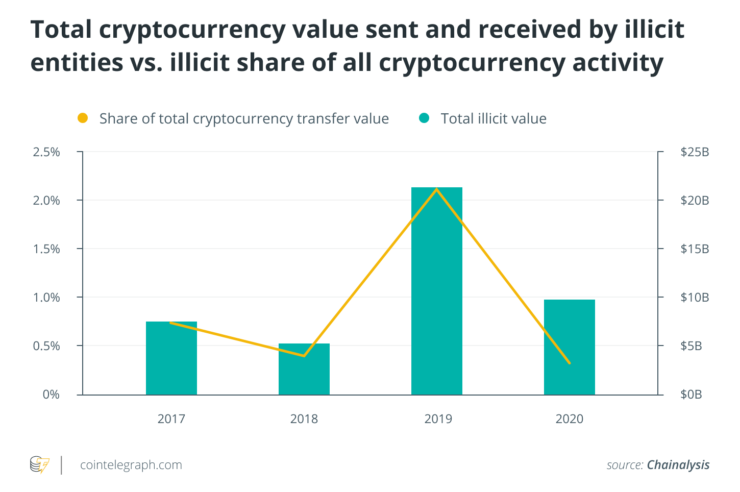

There is no data to support that Bitcoin plays a meaningful role in the transnational money laundering scene. Crypto is also far from being as anonymous as people may think. The fact that a system can be misused does not mean the system should be outlawed; otherwise, we would have long parted ways with banking, cash, fiat currencies, the internet and just about any manifestation of human ingenuity. Yet, we hear the concerns, and we are making sure that in the history books, they will be nothing more than temporary FUD — fear, uncertainty and doubt.

There is another important point on money laundering concerns. We use plenty of tools — such as the sophisticated algorithms of Chainalysis, CypherTrace and Coinfirm — to trace the origins of cryptocurrencies and show a detailed flow of funds. This allows us to draw definitive conclusions on the status of a particular crypto deposit and apply the risk-based AML approach of the FATF. Sure, there are obfuscation tools and cross-chain techniques that make tracking more difficult, but nothing more than what already exists in the banking sector — cross border transfer, offshore jurisdictions, etc.

As someone who has a significant portion of their net worth derived from cryptocurrencies, let me say: Getting fiat currencies from the sale of crypto into the banking system is a Herculean task, so it is the furthest thing from a “money launderer’s dream.” Top tier-one banks require extensive proof of funds from early Bitcoin investors, including, but not limited to, the cryptographically signed messages of the earliest wallets. So, I am not sure how a darknet drug dealer would transfer crypto wealth into the U.S. dollar or euro in any meaningful amounts. Their best hope is to stay within crypto and pay for goods and services with crypto. Sounds similar to the method that the drug cartels have been using since before Pablo Escobar’s days.

Why protect crypto? It’s the only truly free market

In the crypto markets, regulators have something truly unique. The cryptomarket is the only free market, where there is no central bank to engage in interventionist policies, to control interest rates and the money supply. There is no lender of last resort, which in traditional markets has created some moral hazard and has encouraged aggressive long positions. There is no Fed put, no Plunge Protection Team, no bailouts.

In crypto, the market forces of supply and demand and of leveraging and deleveraging get to play out without an arbiter. While this can be dramatic at times, it adds to the antifragility of the space and makes it quick to adapt to new circumstances. While painful for novice investors who come in late to the party and usually with leverage, none of the corrections in crypto cost any government taxpayer money.

This means that crypto cannot be a systemic risk and no company within it can ever be “too big to fail,” which is a net positive for the advancement of innovation. Unlike traditional finance, in crypto, it’s those that develop good products and services that survive.

If crypto has been in a bubble in the past years — and it might very well be — equities have been in a bubbly state for the better part of the last decade. Tesla’s normalized price-to-earnings ratio is 676.35, and as Lyn Alden put it:

“The S&P 500 is arguably the second most expensive it has ever been in absolute terms, which doesn’t bode well for long-term returns.”

But the bubble in crypto should be viewed as a byproduct of the aggressive monetary policy by the world’s central banks and fears of 1970s type inflation, so eloquently said by Paul Tudor Jones, the guy who put “hedge” in the term “hedge funds.”

Related: Forecasting Bitcoin price using quantitative models, Part 2

The future of regulation

There is no doubt that the next Google, Amazon, Facebook or Apple will come out of the crypto space. But for the crypto market to sustain and surpass its current market capitalization of $2 trillion, it needs to continue its path to maturity.

This is why as innovators, but also as licensed institutions, we welcome a constructive dialogue with all key stakeholders of the regulatory process that will ideally translate into clear rules around the way business ought to be structured. It is for the benefit of all involved — regulatory bodies, businesses and retail clients — to have clear guidance and regulatory certainty. This will lead to sustainability, innovation, security of funds, consumer protection, sound AML procedures, and ultimately, more revenue for the jurisdictions that decide to embrace crypto, echoing the United States’ embrace of the internet in the early 2000s.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Antoni Trenchev is the co-founder and managing partner of Nexo, a provider of instant crypto credit lines. He studied finance law at King’s College London and Humboldt University of Berlin. As a member of Bulgaria’s parliament, Trenchev advocated for progressive legislation to enable blockchain solutions for a variety of e-government services, most notably e-voting and the storage of databases on a distributed ledger.

{kind=link}

{kind=link}

Comments (No)