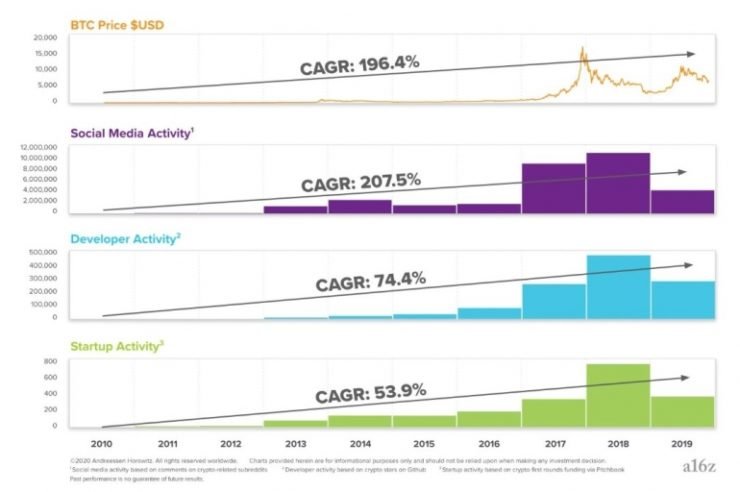

Famed Silicon Valley venture capital firm Andreessen Horowitz (a16z) stirred up some discussion last week by dividing crypto history into cycles that look something like this: The price goes up, which leads to new interest, which triggers new ideas and use cases, which leads to new startups and funding, which leads to product launches that bring in more people. Rinse and repeat.

This would pass as a simple “hunh, cool” if it weren’t for their recent fund raise. Crypto Fund II hoped to reach $450 million; in April, the firm announced that the raise closed at $515 million. Given that the average VC deal size in 2019 was $3.5 million, that’s a hefty amount of firepower with which to kick off the beginning of the fourth cycle.

You’re reading Crypto Long & Short, a newsletter that looks closely at the forces driving cryptocurrency markets. Authored by CoinDesk’s head of research, Noelle Acheson, it goes out every Sunday and offers a recap of the week – with insights and analysis – from a professional investor’s point of view. You can subscribe here.

So why is this raise especially interesting? For four reasons:

1) The fund exceeding its initial target is not the surprising part. What is notable is that it did so right after a year in which VC funding for crypto projects fell by over 50%, according to CB Insights. The slump was not unique to crypto – VC funding across all sectors fell an average of 18% in 2019, according to alternative investment data provider Preqin. The crypto sector was hit especially hard by lackluster crypto asset price movements and the tail end of a bear market. Typical end-of-cycle stuff.

2) This was a16z’s second crypto fund. The first raised $300 million in 2018, the same year the firm also raised $450 million for a second biotech fund, signaling an expansion of its policy of specialization in what it sees as the next areas of high growth.

Crypto funds in a VC structure, however, have a peculiar constraint: they can only invest up to 20% in assets that are not equity of private companies. Since some of the new business models emerging in the space rely on the issuance of tokens which represent equity but are not classified as such, this can limit opportunities to more traditional structures. Not a16z’s style. So, last year it registered all its employees as financial advisers, giving the firm much more freedom in the nature and scope of its investments. It can now invest directly in cryptocurrencies and tokens. And not just from its crypto funds – a16z’s other funds can also now take meaningful stakes in crypto assets. An interesting position to be in at the beginning of a new cycle.

3) So, why raise a dedicated crypto fund rather than, as many other venture capital houses do, just roll crypto-related investments into a general fund? Indeed, a16z started investing in crypto startups as early as 2013, from its general funds. Because crypto-based businesses are usually very different from “traditional” technology plays. It’s not just the technology that requires some understanding (and, trust me, it’s not always easy). It’s also the totally different business models that leverage decentralized incentives and introduce new economic parameters. The familiar technology stack paradigm won’t always apply to crypto businesses.

Specialized crypto venture funds can harness the high-level expertise of their partners, and offer both investors and investees a more bespoke service, which in the fast-evolving crypto asset sector could be the difference between a company making it or not.

On the other hand, investment by general venture funds signals that blockchain-based businesses are becoming seen as technology plays, hinting at an eventual mainstream status. Earlier this week, crypto platform FalconX announced a whopping $17 million pre-seed and seed round led by Accel, which several years ago led the Series A round of a social networking company called Facebook (you might have heard of it).

Other participants in the FalconX round were known venture capital firms such as Lightspeed Ventures (which has also invested in Snap, TaskRabbit and Lady Gaga’s Haus Laboratories), Flybridge (other investments include MongoDB and Codeacademy) and Accomplice (which has stakes in Angellist, Moo and DraftKings, which even a non-sports fan such as myself had heard of). These VCs seem to be betting that a crypto platform will eventually join the ranks of other diverse, well-known names.

Last week saw a similar story: crypto-based shopping rewards platform Lolli raised $3 million from the likes of Peter Thiel’s Founders Fund (Airbnb, SpaceX), Bain Capital (LinkedIn, SurveyMonkey) and Craft Ventures (Reddit, Bird).*

Specialized crypto VC funds harness deeper expertise and allow limited partners to make a more deliberate choice as to where their money goes. Mainstream funds, however, treat crypto investments as one of many exciting new growth areas. With its new registered advisor status, a16z will probably be making bold statements of crypto support from both its specialized and broader technology platforms. The fourth cycle could start to see the blurring of boundaries between crypto and other technologies.

4) Whether through general or specialist venture funds, what these inflows represent is institutional interest in crypto-related businesses. As market observers, we tend to focus on the volumes on crypto exchanges as potential signs of institutional activity. But the range of institutions that are likely to invest directly in crypto assets is relatively small compared to number that can (and do) invest in venture capital. We’re not going to stop monitoring the spot and derivatives markets for signs of institutional activity. But we should also watch the venture funding – that is a sure sign that the institutions are, indeed, here.

It’s also a relatively easy way to track what is likely to be growing institutional involvement in the sector. Most institutions are not allowed to invest in cryptocurrencies directly – they will need to do it through approved vehicles such as venture funds. Also, for many, the volatility inherent in crypto assets is too high. Venture bets have potentially the same upside, without the prospect of sudden changes in valuation.

And, venture investments have greater valuation flexibility, which for many funds is a plus. Valuations of private companies stem from future cash flow expectations and interest rates – one is subjective, the other is historically low and probably heading lower, which should boost valuations and therefore fund balance sheets. In certain categories such as pensions and endowments, this is not just a political expediency, it’s a matter of survival.

Given the growing acceptance of blue-chip institutions and investors such as JPMorgan (which now extends banking services to select cryptocurrency companies) and Paul Tudor Jones, and the overhang of money looking for a return, we could well be entering the golden age for crypto venture capital.

It’s not as dramatic as the crypto asset markets, with wild swings and edge-of-seat narratives. But venture funding implies building, steady progress, support for the never-ending search for product-market fit and a relatively attractive profile for institutions looking for return with reasonable risk. Bring on the fourth cycle. (*Another participant in the round was DCG, CoinDesk’s parent company.)

Anyone know what’s going on yet?

Sentiment is always a strong driver of market valuations, and anyone who’s endured weeks of lockdown can confirm that emotions are swinging more wildly than ever these days. The stock markets’ mood seems to hinge on the likelihood of a vaccine emerging soon – rising when the outlook was promising, falling when a whiff of disappointment crushed unrealistic expectations. Brave is the investor who thinks she can time this well.

What I struggle to understand is that surely the eventual emergence of a vaccine is priced in? Does anyone doubt that we will find one sooner or later? Is the stock market now a play on the timing of that? And even if one emerges tomorrow (which would be wonderful), the world’s troubles won’t necessarily disappear. Let’s not forget that things were looking kind of ropey in terms of growth and income even before the pandemic hit. Apart from the conflicting conclusions on the efficacy of vaccines and testing, there are confusing reports on actual or intended relaxing of lockdowns, and the market does not seem to be taking into account the possibility of second waves. Here in Madrid we now have to wear masks outside, and as of Monday we will be allowed to move around more freely and even visit friends and family in their homes, as long as we don’t crowd more than 10 socially distant people into one room (how big are people’s apartments here?). In the Basque country, they’ve decided to prohibit congregating in private residences, and only allow it in bars. Why not. Meanwhile, this coming week keep an eye on the renminbi, close to its lowest levels in 10 years. The currency was a key leg in the trade tensions that erupted last year. The market seems to be overlooking the recent flare-up, but that could change.

Bitcoin did not have a good week in terms of price, although it is still outperforming other major assets so far this month. The halving last week had the expected effect of lowering the hashrate (which led to a difficulty adjustment downward, which should nudge the hashrate upward again), and has boosted fees considerably. The average USD fee per transaction is now the highest it has been since June 2018.

CHAIN LINKS

Digital currency trader and lender Genesis Global Trading* is moving toward full-service prime brokerage with the acquisition of crypto custodian Vo1t. TAKEAWAY: While many startups have tried to pass themselves off as crypto prime brokers, they have all lacked one important feature: lending. Genesis has experience there, and a strong roster of clients likely to want this service. The advent of real institutional-grade prime brokerage is likely to encourage greater institutional interest in trading and holding crypto assets. (*Genesis is owned by DCG, also the parent of CoinDesk.)

Jeff Dorman at Arca shows that some institutions may be using the CME as a fast and relatively easy way to access physical bitcoins. TAKEAWAY: The volumes of physical delivery in CME bitcoin futures are still minuscule compared to the cash-settled version, but the fact that it’s being used at all is intriguing and worth watching. Crypto asset exchanges in the U.S. are licensed but not regulated, since crypto assets are not yet regulated – the CME is, however, a regulated exchange, which should reassure jittery regulated funds. Plus, most institutional investors already have an account at the CME, so no extra paperwork, collateral, costs, etc. would be required.

Ecoinometrics points out that, while open interest on the CME is growing fast, the average daily volume has stayed within its recent range. This implies a growing degree of exposure and new traders coming into the market. The spectacular growth in CME bitcoin options implies a more sophisticated type of investor is taking positions, and the put-to-call ratio is at an all-time low of 1/20. TAKEAWAY: A reminder that the derivatives markets deserve more attention when it comes to gauging the mood of the market. For instance, most of the call options are betting on bitcoin clearing $10,000 within 10-40 days. However, most of the longs on the CME futures market are from retail investors, not institutional. The “smart money” is still net short.

The CME is not the only exchange with significant growth in options – Deribit, the largest platform in terms of volume for crypto options, has also seen record open interest levels. TAKEAWAY: Strong signals for growing activity from sophisticated traders are popping up all over the place.

Ethan Vera, CFO and co-founder of mining pool Luxor Technologies, shares insights from the FTX difficulty derivative market (I talked about them last week). TAKEAWAY: He believes that they are an interesting trading tool that reveals market expectations of future hashrate. He does not think they are good hedging instruments, since difficulty is just one component of hash price (miners’ daily revenue / hashrate in TH per day) and there are times they have moved in tandem rather than in the opposite direction.

The Financial Times attempted to lift the lid on the volatile and highly leveraged world of crypto funds. TAKEAWAY: The volatile performance of crypto funds is their selling point – high risk, potentially high reward. As March showed, that can produce disastrous results, and the eye-wateringly high leverage available in the sector can exacerbate the negative effects more than it can accentuate the positive ones. As Dan Morehead of Pantera Capital said in the article: “Bitcoin is such high-octane stuff that putting on any leverage is unnecessary.” What Pantera lost in March, it made up in April, which highlights the importance of size, track record and loyal investors.

Bitcoin exchange and custodian Bakkt, backed by NYSE parent ICE, revealed this week that it has onboarded more than 70 clients for its custody services and has partnered with insurance broker Marsh to offer clients more than $500 million worth of coverage. The company is also continuing its work on a retail-focused mobile app after partnering with two unnamed financial institutions. TAKEAWAY: It remains to be seen if Bakkt can pull off being both institutional- and retail-focused – others have tried and failed, as the infrastructure investment and marketing styles are very different. Plus, it will have strong competition in the form of Square’s Cash App and similar offerings.

Crypto Twitter erupted earlier this week with a rumor that some of the original bitcoin mined by pseudonymous creator Satoshi Nakamoto had just moved – implying that 1) he was still alive, and 2) could be about to sell some of his allegedly substantial holding (he was one of the only miners back in the early days). The price fell by 7% over the course of one hour on Wednesday, a move that was in part due to a large and possibly unrelated sell order on Bitstamp, and continued towards a 10% drop to its weekly low of just over $8,800. TAKEAWAY: Many analysts soon refuted that it was Satoshi, and the price started to recover. The interesting part of the episode is the transparency of bitcoin movements, and the fascinating forensics employed to decipher movements.

Last week I pointed out that Brian Brooks, chief operating officer of the U.S. Office of the Comptroller of the Currency (OCC), said that he believes crypto companies could fall under a federal licensing regime rather than state-level money transmitter licenses. This week it turns out that he is being promoted to acting controller. TAKEAWAY: It’s unclear how long this stage will last, and whether or not he’ll be made controller. It’s worth noting that before this position, Brooks was chief legal officer at Coinbase. Let that sink in: the acting controller of the only entity that charters banks in the U.S. used to head the legal team of a crypto exchange.

Coin Metrics shows how changes in the types of machine used to mine bitcoin can impact the network’s security. TAKEAWAY: Take a moment to reflect that it is possible to extrapolate an estimation of the distribution of different types of mining equipment, by looking closely at the blockchain data. That kind of connection between production and information output is quite astonishing.

The Puell Multiple is calculated by dividing the daily issuance value of bitcoins in U.S. dollar terms by the 365-day moving average of the daily issuance value. It is currently just below 0.5, according to the data provided by the blockchain intelligence firm Glassnode. TAKEAWAY: A reading below 0.5 indicates the value of the newly issued coins on a daily basis is quite low compared to historical standards. Historical data suggests that bear markets tend to end with the Puell Multiple’s drop below 0.50.

In case you were looking for something interesting to watch this weekend, Amazon Prime has aired a documentary called “Banking on Africa: The Bitcoin Revolution,” made by South African filmmaker Tamarin Gerriety with sponsorship from the crypto exchange Luno. The film focuses on adoption across the continent, and features interviews with entrepreneurs and educators about the use cases and levels of interest they’re seeing. TAKEAWAY: Volumes are still small yet, but we should keep an eye on evolving use cases in emerging markets. There is where we will see the evolution of bitcoin’s practical applications beyond as an investment asset, which could be key to future valuations. Documentaries like this are a good wake-up call to anyone who says that bitcoin has no “intrinsic value.”

Brazil’s antitrust watchdog, the Administrative Council for Economic Defense (CADE), has voted to continue its investigation of the country’s main banks for denying financial services to crypto brokers in alleged violation of Brazilian competition law. TAKEAWAY: This is similar to the situation in India, where the Supreme Court overruled a ban on banking services for crypto companies. If the CADE rules in the crypto sector’s favor, it could open up a huge market (population over 2 million) that is suffering currency convulsions and intensifying social unrest.

Institutional-grade crypto asset platform FalconX has closed a cumulative pre-seed and seed round of $17 million, let by Accel and participated in by Coinbase Ventures, Fenbushi Capital, Lightspeed, Flybridge, Avon Ventures and others. TAKEAWAY: The size of the round indicates a strong conviction in the growing participation of institutional investors (the firm’s clients must have at least $10 million AUM). This is encouraging – institutional investors bring not only considerable amounts of money, but also legitimacy, and serve as a lead for the rest of financial management to follow. Hedge fund manager Paul Tudor Jones’ recent public comments on bitcoin’s relative value, and the growing volumes on the CME and in Bakkt’s custody business add credence to the anecdotal belief that the institutions are indeed starting to take notice.

Podcasts worth listening to:

(Note: Nothing in this newsletter is investment advice. The author owns small amounts of bitcoin and ether.)

Disclosure Read More

The leader in blockchain news, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies. CoinDesk is an independent operating subsidiary of Digital Currency Group, which invests in cryptocurrencies and blockchain startups.

{kind=link}

{kind=link}

Comments (No)