As the year that felt like a decade on speed starts to draw to a welcome close, some of us are starting to try to make sense of the timeline of narratives and events. Most of us (myself included) are failing. And that in itself is an intriguing narrative, that sheds light on bitcoin’s rally.

Bear with me while I try to explain.

On the one hand, we have a rapid rise in the bitcoin price, and coalescing institutional support from traditional investors and companies that see potential in crypto assets and markets.

On the other hand, we have conflicting economic and social trends. We have blind faith in the power of vaccines combined with rejection of the science of virus transmission; monetary policy designed to encourage lending combined with banks that are unwilling to do so; growing interest in the value of emerging markets combined with escalating risk of default; widening inequality combined with greater power of protest; I could go on …

These conflicting forces and the uncertainty swirling around them should encourage us to look closely at prevailing narratives. Yet those of us watching the growing institutional interest in bitcoin markets have accepted without question the assumption that bitcoin’s inflation hedge qualities are behind it.

Let’s pick that apart.

The deflation debate

First, let’s look at another pair of conflicting economic trends.

Most economists seem to believe that a resurgence of inflation is unlikely. Depressed consumption and excess supply, the continuing impact of technology and demographic shifts, the low velocity of money and the weak labor market are just some of the factors they point to. These have already led to deflation in some key economic areas.

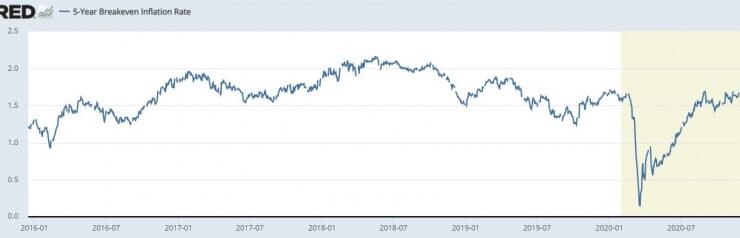

The bond market, on the other hand, tells us that inflation concerns are real. The five-year breakeven rate, a proxy for inflation expectations calculated by taking the difference between five-year U.S. Treasurys and Treasury Inflation-Protected Securities, is close to its five-year high.

What’s more, the yield curve continues to steepen, signaling expectations of higher interest rates in the future as central banks tackle a looming inflation problem. Taking into account the damage rising interest rates would do to debt-laden economies, this is the bond market telling us that they see trouble ahead.

An inflation hedge

But does that really matter for bitcoin?

Bitcoin is seen as an inflation hedge mainly because of its limited supply, which is not influenced by its price, and because of its relative attractiveness when real yields head to zero or lower.

Yet when you buy bitcoin, you’re not just doing so to hedge inflation. You’re buying bitcoin to hedge all the other negative consequences that usually accompany it.

True, inflation is not always bad. “Good” inflation, a result of economic growth and low unemployment that helps to close the gap between supply and demand, encourages investment and even more economic growth.

Runaway inflation, however, exacerbates poverty, heightens uncertainty, demolishes trust in institutions and can lead to the breakdown of social order. This is not isolated to post-WWI Germany – we see it today in Venezuela, Zimbabwe, Lebanon and Argentina, to name just a few.

Bitcoin is also a hedge for unstable governments that close bank accounts, police states that want to seize private wealth, broken payments rails due to corrupted systems or outside cyber attack threats, paranoid leaders that want to disenfranchise opponents, export-protecting devaluations that trigger more inflation …

These are less likely in developed economies. But let’s not forget that tipping points lurk around unexpected corners, and that Venezuela was once one of the wealthiest countries in the world and one of the more stable democracies in Latin America.

Bitcoin is a hedge against inflation, but also against political instability and social disruption, which – if inflation comes roaring back – is not a ridiculous thing to prepare for.

A dollar debasement hedge

Bitcoin is also a hedge against a more gentle but just as pernicious debasement of currency through a loss of trust.

Traditionally, inflation moves in tandem with the strength of the local economy. But it can be triggered by currency weakness, which raises the prices of imported goods.

This is usually corrected when the central bank raises interest rates to combat rising inflation, which increases the attractiveness of the currency compared to others.

But in the current environment, an increase in interest rates may have the opposite effect, given the potentially catastrophic impact on debt-ridden economies. The U.S. bond market is telling us that it thinks interest rates will rise. The dollar continues to head lower, however, and could continue to do so even if those rate increases materialize, as faith in the capacity of the U.S. to employ traditional tools to good effect could be shaken.

And, most bitcoin trading is denominated in dollars. Therefore, if the dollar heads lower without a corresponding fall in the value of bitcoin (and since it’s unrelated to the economy, there’s no fundamental reason why it would), the BTC/USD ratio heads up.

Bitcoin is a hedge for not just the macroeconomic ills that we have been trained to watch out for. It can also provide ballast against the unforeseen problems waiting to be triggered.

The ‘crazy’ thesis

This highlights another hidden strength of bitcoin as an investment asset.

It is unlike any asset that we have seen before: programmatic supply, decentralized governance, fragmented market infrastructure that runs on technology developed by an unknown entity yet maintained by miners, developers and validators distributed across many geographies.

It doesn’t fit into standard economic thinking – and for that reason, it is perfect for our times.

In a world where you’ve gone from orthodox monetary policy to Keynesian economics to MMT in a few months, there is no longer any trust in the traditional recipes.

To paraphrase G. K. Chesterton, when you stop believing in traditional recipes, your mind is more open to new ones.

Bitcoin in portfolios represents more than a new recipe. It represents the need for a new recipe. It represents a safety play against a world in which old ideas are up in the air, and new ones have yet to take root.

It represents more than a hedge against inflation: it also represents an acceptance that politics and economics can get weird, and that untested ideas that are untethered to macroeconomic features and past assumptions are worth considering.

It represents a hedge against “crazy,” which is hopefully not what awaits us – but the risk of not preparing for that possibility is verging on irresponsible, and not even thinking about it is likely to end up being prohibitively expensive.

Anyone know what’s going on yet?

The outperformance of bitcoin in 2020 has to set up the asset for even more professional investor attention next year, even though we all know that past performance is not an indicator of future performance. Or is it? The momentum trade seems to be the predominant strategy this year, and given the amount of money sloshing around markets looking for a good return, there is no indication that will end soon.

Then again, all bull markets have to end some time, although the underlying fundamentals and investment theses of bitcoin do not get worse with vaccine disappointments and worse-than-expected economic figures – unlike with stock and bond markets.

CHAIN LINKS

Investors talking:

· Scott Minerd, CIO of fund manager Guggenheim Partners, which manages more than $230 billion worth of assets, told Bloomberg TV hosts this week that his firm’s fundamental analysis shows that bitcoin should be worth $400,000. This conclusion is based on the asset’s scarcity, and its relative value to gold as a percentage of gross domestic product. He also revealed that Guggenheim had started allocating to bitcoin when it was trading at around $10,000.

· U.K.-based fund manager Ruffer Investment Company has invested approximately $740 million in bitcoin, equivalent to around 2.7% of the firm’s assets under management. According to the company, the investment was “primarily a protective move for portfolios” to “act as a hedge” against “some of the risks that we see in a fragile monetary system and distorted financial markets.” Ruffer is known in investment circles as a conservative manager focused on capital preservation. It had the top-performing active fund in Europe for Jan-June 2020: the LF Ruffer Gold Fund produced a six-month performance of over 55%. And now it’s investing in bitcoin. Ruffer has spoken often in the past about its inflation concerns. This investment makes me want to check in on other active managers worried about inflation – their ranks are growing.

· One River Asset Management, a $1 billion hedge fund (as of April 2020) specializing in volatility plays, has invested $600 million in bitcoin and ether for institutional clients (including Ruffer, which owns a stake in the company) via its subsidiary One River Digital Asset Management. CEO Eric Peters told Bloomberg that One River Digital’s crypto holdings will cross $1 billion in early 2021. Brevan Howard Asset Management co-founder Alan Howard is taking an ownership stake in One River Digital and helping to provide the company with back-end trading services.

· Christopher Wood, global head of equity strategy at investment firm Jefferies, has trimmed the recommended exposure in his model global portfolio from 50% gold in favor of bitcoin. This is even more notable given that this particular portfolio is designed with U.S. pension funds in mind. What’s more, he has said that he plans to increase exposure to bitcoin should there be a correction.

· Jeff Currie, head of commodities research at Goldman Sachs, told Bloomberg that bitcoin was a “retail inflation hedge,” and a risk-on growth proxy.

· Not an endorsement, but an interesting and potentially useful thread prompted by tech investor Andrew Wilkinson, co-founder of Tiny Capital.

In market developments:

U.S.-based crypto asset exchange Coinbase has filed preliminary documents with the U.S. Securities and Exchange Commission (SEC) to go public. The Form S-1 is expected to become effective after the SEC completes its review process, subject to market and other conditions. TAKEAWAY: Here we go … This will create by far the largest listed company in the crypto industry, and has been rumored for some time. As well as attracting even more attention to crypto markets, it is likely to kick off a slate of crypto-related listings, especially given the recent price movements and the swelling of institutional interest. What I’m most excited about, apart from seeing how the market values a systemic crypto market infrastructure business, is getting a look at their balance sheet and P&L.

Cboe Global Markets will launch a suite of crypto market tools in 2021 in a licensing partnership with execution provider CoinRoutes, including cryptocurrency indexes, historical data and real-time ticks. TAKEAWAY: Cboe operates the largest options exchange in the U.S. Coming from a traditional market infrastructure player, this deal signals support for the nascent asset group, and points to the introduction of new crypto services and products over the coming years. S&P also recently revealed crypto index plans, and other market data providers are likely to join the race to capture crypto data market share.

The Chicago Mercantile Exchange (CME) will launch a futures contract on ether (ETH) in February 2021. TAKEAWAY: This goes a long way towards validating ETH as a potentially institutional-grade investment. The lack of liquid ETH derivatives for institutional investors has dampened hedging opportunities, and the removal of these barriers could encourage more professional investors to at least consider its merits.

Advisory company Evercore has named PayPal as its top payments stock, in part because it believes that the firm’s cryptocurrency services could be good for customer engagement and transaction margin. TAKEAWAY: This not only encourages investors to consider companies that are launching crypto asset services; it also encourages more companies to offer crypto asset services, because who doesn’t want investors looking at them?

Sovryn, a self-billed “decentralized platform for trading and lending Bitcoin,” has launched on the Bitcoin sidechain RSK, with $2.1 million in funding. TAKEAWAY: There’s a lot of debate about whether Bitcoin could ever be used for smart contracts. This is a reminder that the jury is still out, and technological progress is pretty good at showing that what many think is impossible is not that impossible after all. If the range of applications that can be built on Bitcoin broadens, that could boost its potential value.

SBI Financial Services, the subsidiary of Japanese tech conglomerate SBI Holdings, has acquired U.K.-based cryptocurrency OTC desk B2C2. TAKEAWAY: This is another example of legacy finance leveraging crypto asset services to broaden its client base, and to sell more to existing clients.

Banca Generali, an Italian private bank that focuses on wealth management for high net worth individuals, is leading a $14 million investment round in crypto wallet provider Conio, with an agreement to offer Conio’s services to the bank’s clients. TAKEAWAY: Yet another legacy bank gears up to offer crypto asset services to its clients. We will see a lot more of this in 2021.

You have banks building or buying crypto asset services, and you also have crypto firms trying to become banks. Crypto payments firm BitPay has filed to become a national bank in the U.S., headquartered in Georgia. TAKEAWAY: By becoming a national bank, BitPay will be able to operate in all U.S. states, while its non-bank competitors will need to get money transmitter licenses in each state they wish to operate in. This confers an operational advantage, and also a strategic advantage in that clients could prefer the additional scrutiny borne by national trust banks, compared to firms that don’t have a national bank license.

Speaking of crypto firms hoping to become banks, crypto asset platform Paxos (which last week filed to become a federally regulated bank) has raised $142 million in a Series C round. TAKEAWAY: Paxos is emerging as a key player in the developing crypto market infrastructure: as well as a crypto exchange itBit, it is building a full-stack infrastructure service that includes custody, tokenized securities, stablecoins and more. It powers PayPal’s new bitcoin offering, and also counts Credit Suisse, Société Générale and Revolut among its clients. (Paxos’ founder, Charles Cascarilla, was named one of CoinDesk’s Most Influential for 2020.) With this amount of funding, it will be interesting to see which of their many services they choose to build out more, or whether they will be adding new market tools to the mix.

{kind=link}

{kind=link}

Comments (No)