Digital assets, as a new asset class, exhibit interesting characteristics that could benefit a diversified portfolio of traditional assets. There are, however, many ways to get exposed to digital assets — passive investment, actively managed, short or long term investing, etc. — and with over 800 funds of all sizes, ranging from passive index to active trading funds to venture capital funds and fund of funds, it can be hard to sort the wheat from the chaff.

Just like hedge funds, crypto funds come in all shapes and sizes, and investors tend to look at them through their usual hedge-fund analysis prism. However, as crypto funds deal with a new asset class that has unique characteristics — digital assets — investors can be led to misleading conclusions when traditional asset metrics are used.

The purpose of this article is to provide a quantitative analysis framework to get a first sense of a crypto fund. This is a simple set of tools that helps to understand the potential risk and possible upside of a crypto fund, but no investment decision should be only made on them. One may use these tools to screen a list of crypto funds from a database and extract a short-list to be reviewed in-depth or to assess more precisely a selected crypto fund.

Short-listed funds should then be assessed for their noninvestment strategy aspects — i.e., their operations, their team, their service providers, etc. — which are out of the scope of this article. Also, please note that this is not the de facto method to analyze funds, but only one that has proven its robustness over time.

Different kinds of funds

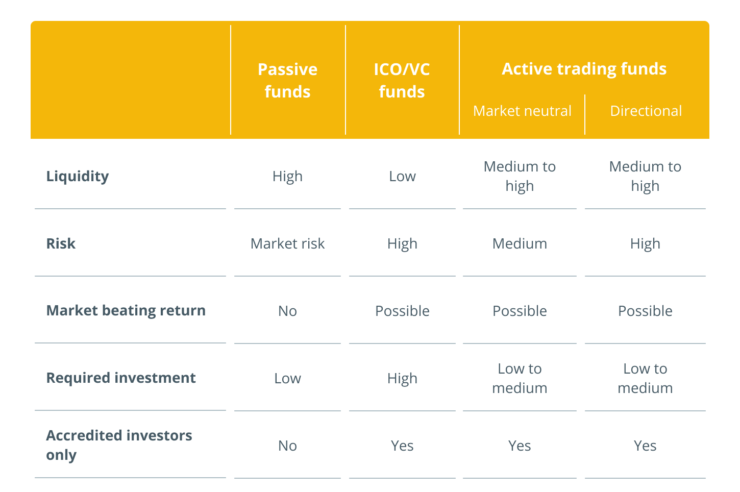

Passive index funds. These funds provide passive exposure to a single or a basket of digital assets in an easily investible format — fund or certificate — where the value is linked to the underlying minus fees. Most of such funds will hold the physical assets (such as Grayscale Investments), but others provide the exposure — essentially, to Bitcoin (BTC) — through futures contracts, which are derivative instruments linked to the value of the physical digital assets. They deliver the performance of the underlying asset held, and typically have higher daily-to-weekly liquidity and lower fees.

Initial coin offering/venture capital funds. These funds invest essentially in early-stage companies via the detention of company-emitted tokens instead of traditional shares of the company but without equity ownership and right to future dividends. These funds are not different from traditional venture capital funds: They invest in a basket of promising projects and look to resell their ownership when the projects have matured, splitting their investment risk on various projects instead of just an “all-or-nothing” strategy. Their liquidity terms for investors tend to be better than traditional VC funds/private equity firms, but they are still highly dependent on the liquidity of the underlyings.

Active trading funds. This category can be split into two sub-categories: (1) market-making/market-neutral funds that provide exchanges liquidity; and (2) directional-trading funds. Funds from the first sub-category tend to deliver a steady performance by sharing the profits they make by acting as the counterparty to traders on exchanges charging a small fee for their service; whereas funds from the second sub-category tend to deliver a more volatile performance than the market-neutral funds but in exchange of a generally much higher performance over the mid-to-long term.

Market-making/market-neutral funds tend to be fully automated due to the very large amount of trades taken in a short period of time, but directional trading funds can be either discretionary — i.e., investment decisions are human-based — or systematic where investment decisions result of a human-designed model but executed by a computer for the best efficiency.

Selecting a crypto fund

Passive index funds

For an investor simply looking to get exposure to a hard-to-store asset such as digital assets, a fund providing passive exposure is the best option as long as the fund custodies the physical digital assets and could provide “in-kind” redemptions — i.e., the fund could return the investors’ money in the form of physical digital assets, as well as in equivalent fiat currency.

Funds that provide passive exposure to digital assets through futures are the worst option. Because futures have to be “rolled” on a regular basis, extra costs are incurred, including trading costs, execution slippage and “roll” costs, which can be seen as extra management fees, eating the investors’ investment value over time independently of the underlying returns.

Moreover, since such funds don’t hold any physical asset, they cannot deliver them “in-kind” directly; if they provide the option, that would come at an extra cost to the investor, as the fund would have to purchase the physical digital assets on the market in order to deliver them to the investor — for a value less than their market value when all purchasing costs are accounted for.

ICO/VC funds

Investing in such funds is very difficult, as no one has a crystal ball to predict what early-stage projects are going to be the next unicorn. Investors can only rely on the experience of the fund management team in selecting projects and their means to strengthen and develop them. Picking up the next unicorn could lead to an astronomic return on investment, but it will take time.

Investing in such funds can provide uncorrelated returns versus the broad market, but during global bear markets, the valuation of these projects tends to fall as well, and so does the value of the funds.

Active trading funds

Funds that are neither passive index nor VC funds can be considered active trading funds. It is mandatory, first of all, to have a fundamental understanding of the management investment strategy: Will it be more market-making/market-neutral or directional? Long/cash or long/short? Systematic or discretionary? What universe of instruments are traded? And so on. This sheds light on the general framework of the fund.

Market-neutral funds tend to exhibit a steady performance — i.e., low volatility and low drawdowns — but can appear very remote from the digital assets returns, whereas directional funds tend to exhibit a higher return but at the price of higher volatility and deeper drawdowns.

Market-neutral funds

Market-neutral funds are generally easier to assess than directional funds, as their performance is expected to be as steady as possible: the steadier, the better.

However, before investing in a market-neutral fund that exhibits the highest expected performance among its peers, given an acceptable level of returns steadiness, the investor has to understand what could possibly go wrong with the fund strategy. For a market-making high-frequency trading fund, it could be an IT issue or some dislocation in the broad market, leading to very large spreads impacting the market-making algorithm (see the notorious 2010 flash crash).

Since their performance is generally much lower than directional funds but are much steadier, an investor can be tempted to leverage investments in such vehicles. However, the investor has to keep in mind that there is no guarantee of steady returns, and leveraging several times such funds could lead to an unexpected, drastic loss should something go wrong.

Indeed, even if market-neutral funds exhibit a very low net exposure, it doesn’t mean that they have a very low gross exposure; they can be levered on the long and the short side many times, which may lead to a very sudden, huge loss (see 2007 Quant Quake for a more academic analysis).

Directional funds

Directional funds, contrary to their market-neutral cousins, try to capture market moves being either long (during market up-moves) or short (during market down-moves) for funds having the ability to play both sides of the market (long/short funds), whereas the long/cash funds will try to only capture market up-moves while remaining in cash during downward market moves.

Directional funds are much more volatile than market-neutral funds, and their drawdowns could be significant, especially with cryptocurrencies.

Discretionary vs. systematic directional funds

Assessing a discretionary, human-managed fund is harder than assessing a systematically computer-driven fund.

Past track record. The past live track record of a discretionary fund may not reflect its future performance, as the fund manager took some trading decisions along the way according to the market environment back then and may not take similar decisions going forward. However, a systematic fund implements a set of trading rules applied by a computer, guaranteeing that the output will always follow the same investment process as far as the fund manager doesn’t change the model nor override the model decisions.

Backtest. The backtest of a fund is a simulation of the trading rules as if they had been applied in the past. For obvious reasons, a backtest is inherent to systematic funds as the investment process has to always be the same. Despite all of the caveats of a backtest (like any simulation), if it has been established under reasonable hypotheses, it can give some insights about the expected performance of the manager going forward. Detailing all of the potential caveats and how to estimate the value of a backtest is beyond the scope of this article, but one quick check that can be done is to compare the backtested results vs. the realized results over the same period. The more in-synch the two track records are, the more robust and insightful the backtest. However, if the two track records diverge, some questioning of the manager prevails.

24/7 markets. Crypto markets are open 24 hours a day, 7 days a week, in contrast to traditional asset markets, which are open only a few hours a day and not on weekends. Therefore, a crypto fund manager must always be on the lookout, as swift moves can occur without much notice at any time during the day — much like how Bitcoin lost 50% of its value in less than two hours on March 12, 2020. So, only the most reactive investment strategies will be able to trade.

Therefore, a discretionary directional trading crypto fund has to be managed by a team of at least three portfolio managers relying on each other every eight hours to monitor the markets and trading accordingly, as well as a couple of extra portfolio managers as substitutions for the main ones, but nothing guarantees that the different portfolio managers would react the same in a given situation.

On the other hand, a systematic computer-driven fund, if properly designed with strong oversight and risk-management processes, can run 24/7 and be simply monitored by a small team. This is why most of the directional trading crypto funds are systematic and computer-driven.

This is part one of a two-part series on how to sort crypto funds — read part two on how to analyze actively trading crypto funds with some useful metrics to assess their true risk here.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, you should conduct your own research when making a decision.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

David Lifchitz is the chief investment officer and managing partner at ExoAlpha — an expert in quantitative trading, portfolio construction and risk management. With over 20 years of experience in these fields and 8+ years in information technology with financial firms, he has notably been the former head of risk management at the U.S. subsidiary of Ashmore Group, which had $74 billion in assets under management in 2018. ExoAlpha has developed proprietary, institutional-grade trading strategies and infrastructure to operate seamlessly in the digital asset markets applying strong risk management principles.

{kind=link}

{kind=link}

Comments (No)