Ethereum (ETH) demand is largely driven by the token’s use in on-chain applications and token transfers, according to a report by CoinShares.

Ethereum’s Use-Cases Have Increased, But Long-Term Value Is Missing

In a recently published detailed report, CoinShares’ Matthew Kimmell noted that despite Ethereum’s potential to host popular applications in the future, investors are struggling to see a significant value proposition in its native ETH token.

Related Reading

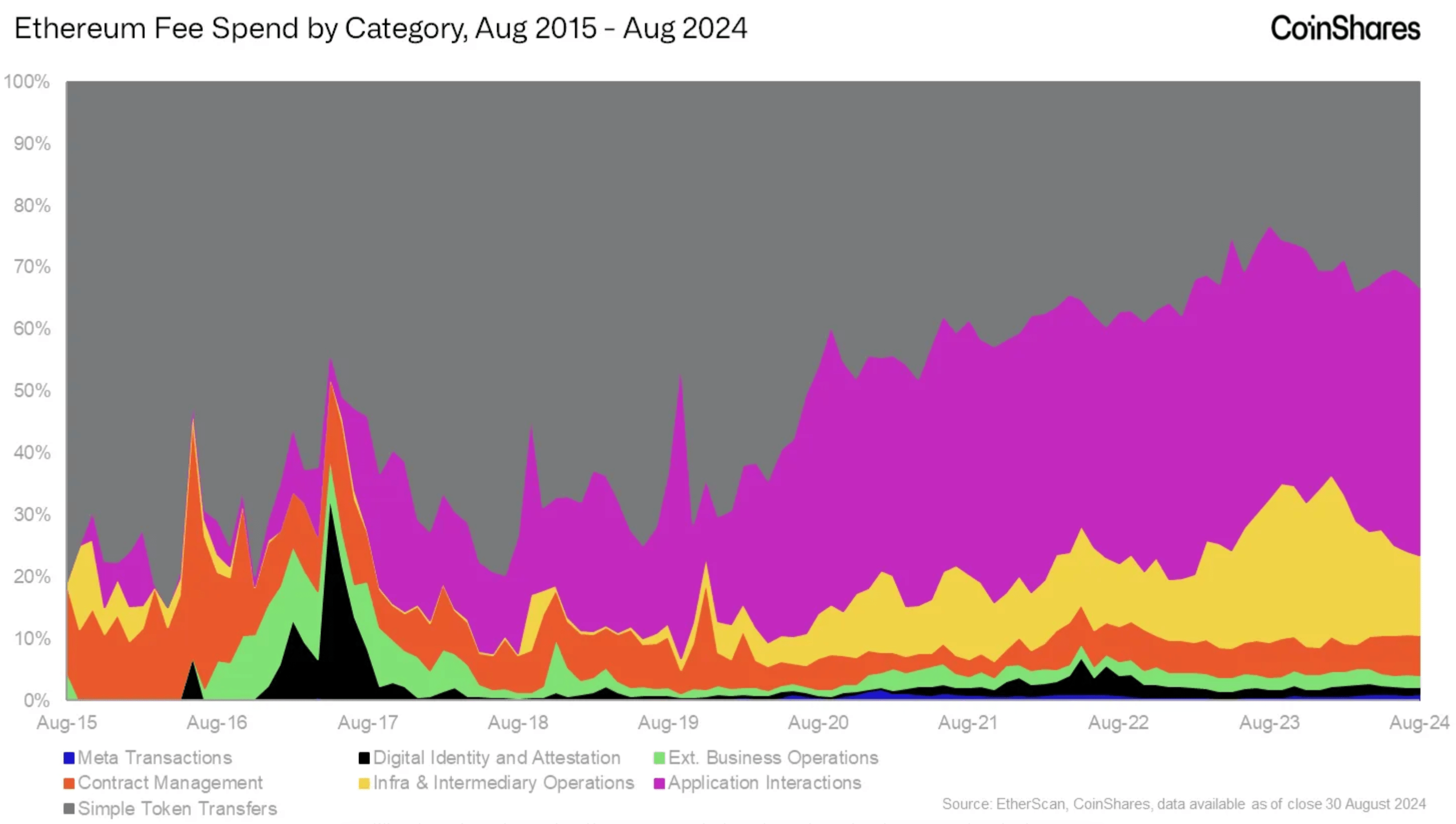

Since its inception in July 2015, Ethereum has made big strides as it has continually witnessed the emergence of new use-cases, starting from simple token transfers, to use in on-chain applications, decentralized finance (DeFi) protocols, and, most recently, non-fungible tokens (NFTs).

According to the report, Ethereum began to see broader utility from 2018 onwards, when its major use shifted from token transfers to simple on-chain applications, digital identity systems, and on-chain withdrawals.

From 2020 onwards, Ethereum has facilitated more complex use-cases such as protocol staking, liquidity mining, MEV (maximum extractable value), bridges, oracles, and second-layer technologies. Although the increasing use-cases might sound favorable for Ethereum at the surface level, the challenge lies in ETH usage being concentrated among a limited range of services.

The report reads:

However, the hard truth is that a very small set of services consistently makes up the majority of Ethereum usage, and these sets largely revolve around speculation or simple value transfer, not necessarily the type of complex “real-world utility” use cases originally envisioned by the developers of the Ethereum Foundation.

The chart below confirms this observation, showing that simple token transfers and application interactions comprise the bulk of ETH usage, followed by infrastructure, intermediary operations, and contract management.

Marketplaces Dominate Application Usage, Stablecoins Lead Token Transfers

The report highlights that on-chain marketplaces – especially decentralized exchanges (DEXes) like Uniswap – dominate application interactions. Notably, over 90% of transaction fees originate from marketplace activity.

In the first half of 2024, Uniswap alone captured about 15% of Ethereum transaction fees. This is not surprising, as the leading DEX recently achieved the milestone of generating $50 million in revenue. On the contrary, NFT trading platforms have suffered a dramatic decline in user transactions since their peak in 2021.

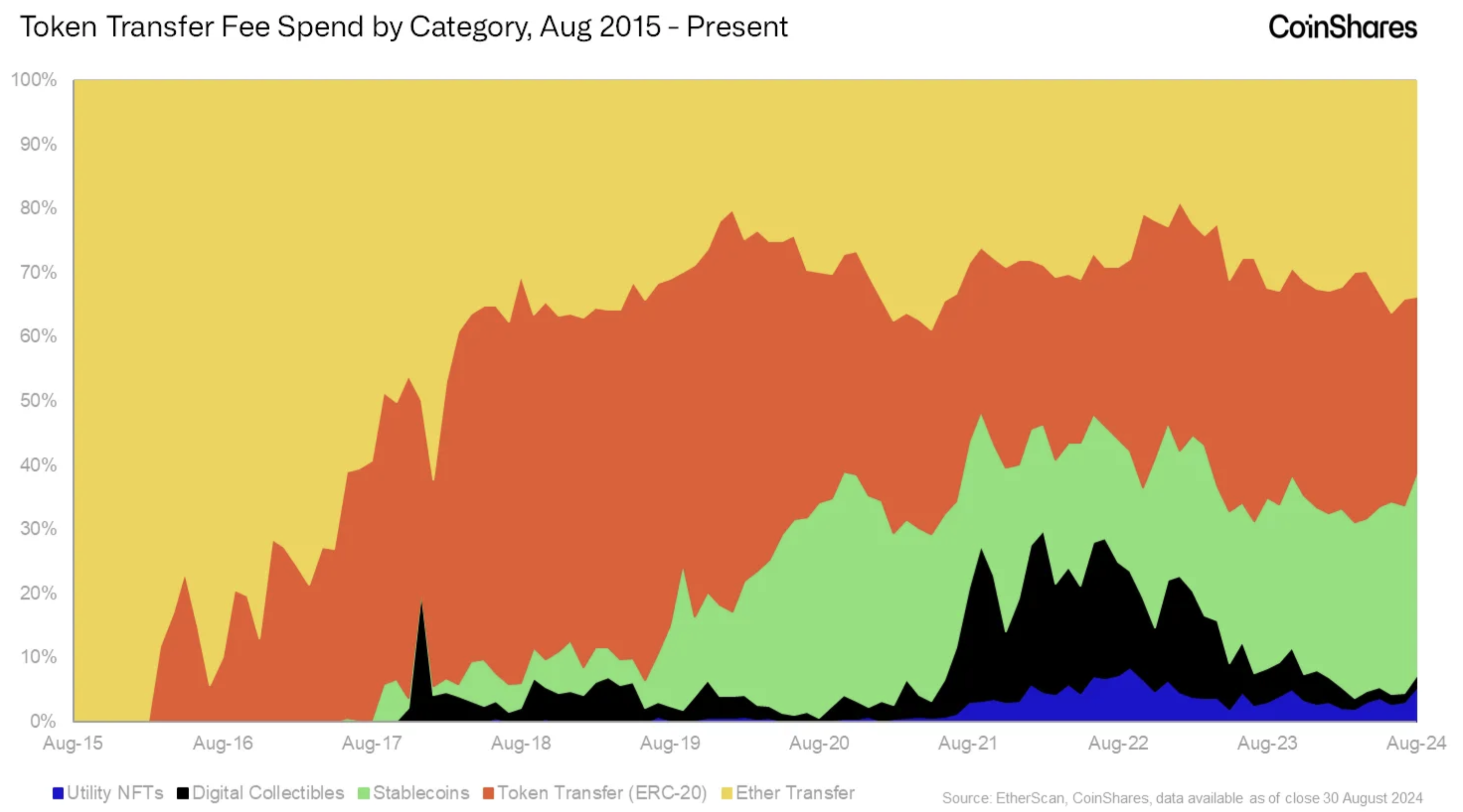

Token transfers continue to play a key role in the Ethereum network activity. With the constantly expanding ecosystem, the type of tokens being transferred has diversified. However, ETH, and stablecoins such as USDT and USDC have emerged as the dominant tokens in terms of transaction fees.

The chart below illustrates the rise of stablecoins from mid-2017, when USDT began to see high adoption as a trading pair for almost all listed ERC-20 tokens on crypto exchanges. Circle’s entry into the market in late 2020 with its USDC stablecoin further boosted stablecoin usage within the wider Ethereum ecosystem.

An interesting observation made in the report is regarding the increased use of Ethereum layer-2 solutions. While their adoption has tackled some of Ethereum’s scalability issues, they have also, unintentionally reduced demand for Ethereum’s base layer. Kimmel notes:

In our view, the latest major change, EIP-4844, which strongly incentivized Layer 2s, has worked directly against the economic design benefits of EIP-1559, which tied the value of ether to its Layer 1 platform demand.

Related Reading

ETH trades at $2,613 at press time, up 0.2% in the last 24-hour period. Stablecoins such as USDT and USDC command a market cap of $119 billion and $36 billion, respectively.

Featured image from Unsplash, Charts from CoinShares.com and Tradingview.com

Comments (No)